The world food market is currently undergoing another crisis. Prices for food commodities (FCOs) surged to April 2026 levels not seen since January 2024 after the total closure of the Strait of Hormuz in late February. In April 2026, the World Bank reported that the food prices in the April 2026 report had increased by 5% in the two months from the conflict’s onset compared to the prior two months. Though this may appear to be a small number, the food system is in an emergency. On a global scale, food systems are fragile, and the emergency is ongoing. The real question is what makes the food systems so fragile to geopolitical changes.

In the last week, supply chain disruptions to grain have been leading to food systems in a critical emergency, though nowhere near the grain supply disruptions in Ukraine in early 2022, when supplies were cut in a single day.

Instead, the disruption is moving at a different pace, via rising energy costs, rising fertilizer costs, and rising transport costs. Its near closure of the oil-rich Strait of Hormuz, through which much of the world's oil supply passes, caused oil prices to escalate rapidly and pass along through all phases of the agricultural supply chain.

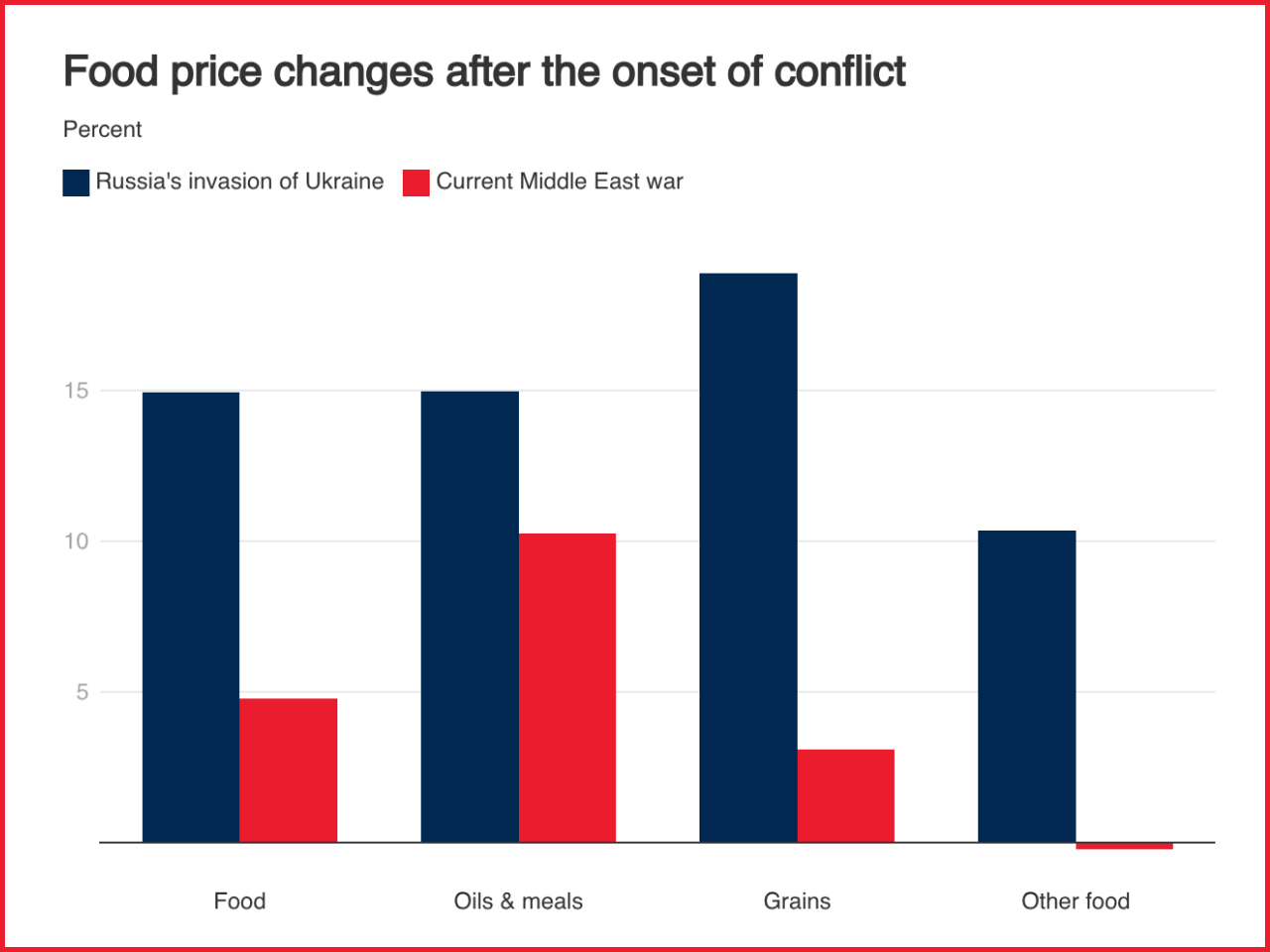

This is an important difference. The 15 percent rise in food prices in the same period of the year up to 2022, compared with the previous year, was about three times higher, following Russia's invasion. This time, the answer was more circumscribed since worldwide stocks of grain and oilseeds are ample, and many northern hemisphere farmers were able to buy fertilizer stocks first, before the conflict. The immediate shock is thus one of the cost escalations and not of the elimination of supplies, but that does not diminish or lessen the impact on the world's most vulnerable groups.

The state of world grain supplies is one of the most important stabilizing factors in the current environment. In 2025–26, global grain stocks are expected to be at a record level, providing a buffer that is sufficiently limiting the food price reaction. Notwithstanding this benign supply situation, the prices of grains increased by 5 percent during the first quarter of 2026 over the previous quarter, driven by the upward movements of prices of grains, which were 9 percent during the period. The rises are driven by drought fears across major production areas, declining spring planting forecasts as a result of higher fertilizer prices, and logistical impacts across global trade routes. Oils and meals have suffered the most from the current disruption of all food commodity groups. The following 2 months, in the period immediately after the beginning of the conflict, prices in this group increased by 10 percent, up to April 2026, the highest in the past two years. At this time, the oils and meals index had already risen by ten percent from the same time a year ago. Two factors were responsible for the rise: high crude oil prices made biofuels a more competitive option, and increased biofuel blending mandates in the largest economies, such as the USA, Thailand, and Indonesia. Among the standout movers, soybean oil jumped 16 percent, quarterly, and 25 percent year-on-year, driven by U.S. renewable diesel targets that were released as part of the fiscal measures by the U.S. Congress in late March. Soybean prices also advanced due to strong demand for vegetable oil and renewed purchases by the Chinese importers. Biodiesel demand was the main catalyst for the firming of palm oil, as well. But in the end, there were still plenty of edible oil stocks around the world to dampen further price surges.

The most worrying aspect of the ongoing crisis is its effect on food security in the most vulnerable areas. This was quickly reversed by the closure of the Strait of Hormuz. Food inflation surged in Gulf economies in March, which rely on imports and sea transportation routes to a large extent. Among those who suffer from food inflation, the Islamic Republic of Iran is one of the hardest hit, with inflation rates already soaring at 98 percent in February 2026. The food inflation rate not only accelerates in the Middle East, North Africa, Afghanistan, and Pakistan (MENAAP) region. This pattern of rising prices was especially found in Europe and Central Asia, in Latin America and the Caribbean, and in South Asia, echoing that seen in the 1 month following Russia's attack on Ukraine. With continued serious supply disruptions from mid-2026 and oil prices at $100 or more for a longer time, about 45 million more people would experience acute hunger during the year, according to the UN World Food Programme (WFP). Over half of the at-risk people are found in Sub-Saharan Africa and the MENAAP.

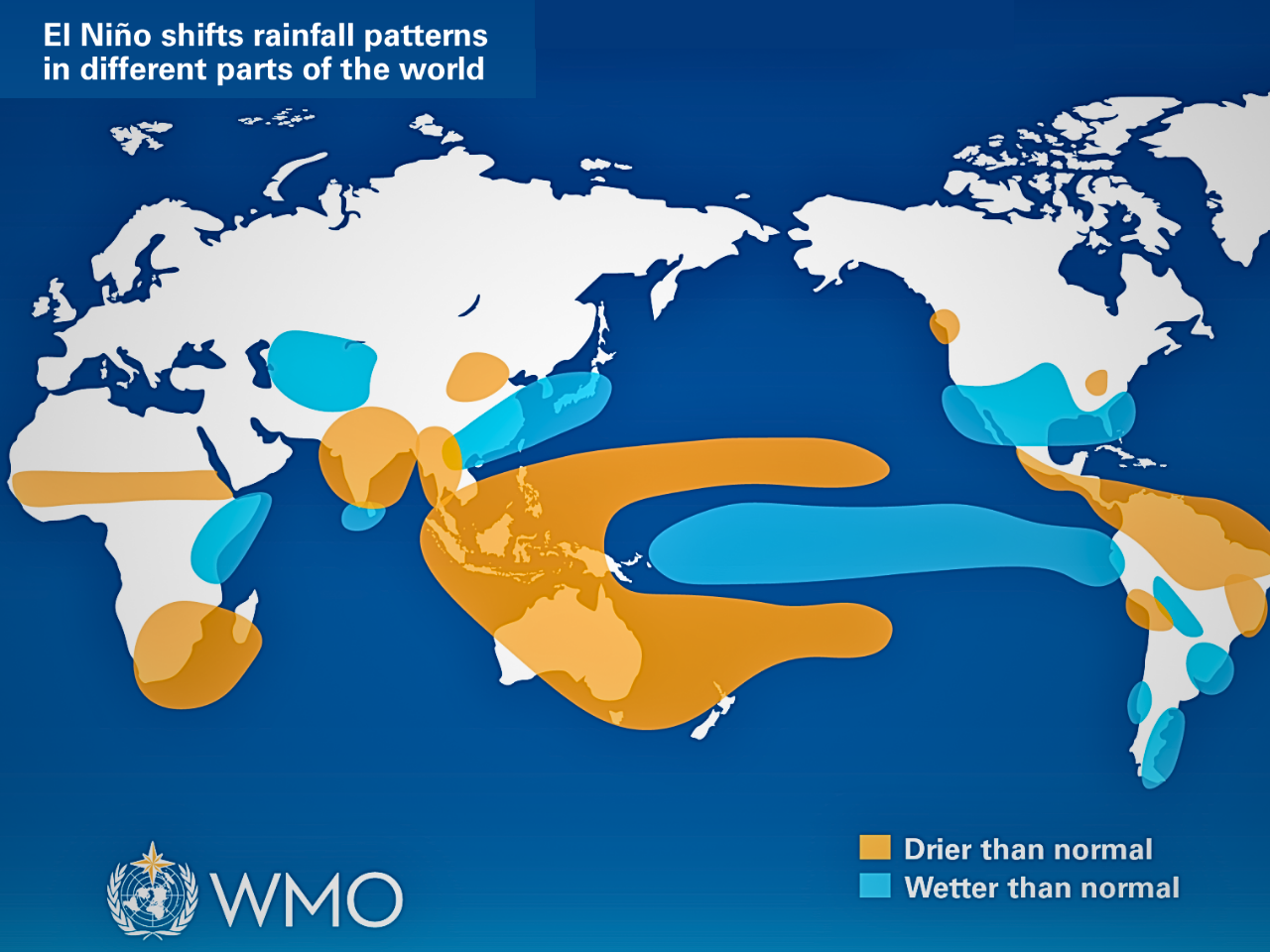

The World Bank's baseline food price projection is based on a ‘return to normal' in supply disruptions in the Middle East beginning mid-2026. It is assumed under this scenario that prices for food commodities will increase slightly (around 2 percent) for grains, 4 percent for oils and meals, and 2.5 percent for the overall food index in 2026. These are reasonable expectations, as long as the assumptions remain unchanged. The risks are, however, decidedly one-sided. This could lead to much higher food prices for the rest of the year if the fighting escalates beyond mid-year and energy and fertilizer prices remain higher for longer. If one develops, it would make matters more difficult if a stronger-than-normal El Niño event were to occur, as it would damage the crop in several producing areas at once. In the months to come, the key to global food markets will be whether supply disruptions abate as posited by the baseline. The April 2026 Commodity Markets Outlook is an invaluable reminder that while record stocks ease, they still do not buffer global food markets from geopolitical events. But the present crisis is being experienced most strongly not in terms of crop loss but by the gradual, stealthy push up the chain of agricultural supply. The primary and most urgent concerns for policymakers must be twofold: first, to support diplomacy to achieve stability of the main supply routes, and second, to help support food safety nets in the most vulnerable economies to food price volatile imports. Food crises have occurred in the past, but the margin for error is diminishing with each food crisis.