Since the 2008 financial crisis, the world has made some progress towards a more balanced and fair global trade system, but that progress has now reversed. Largely ineffective and, in some cases, damaging to economic welfare are the world's favorite political fixes, tariffs and industrial subsidies, the International Monetary Fund warned in a pointed new policy paper. The Fund's key message is clear: rebalancing is not about putting up trade barriers but about coordinating domestic macroeconomic reform.

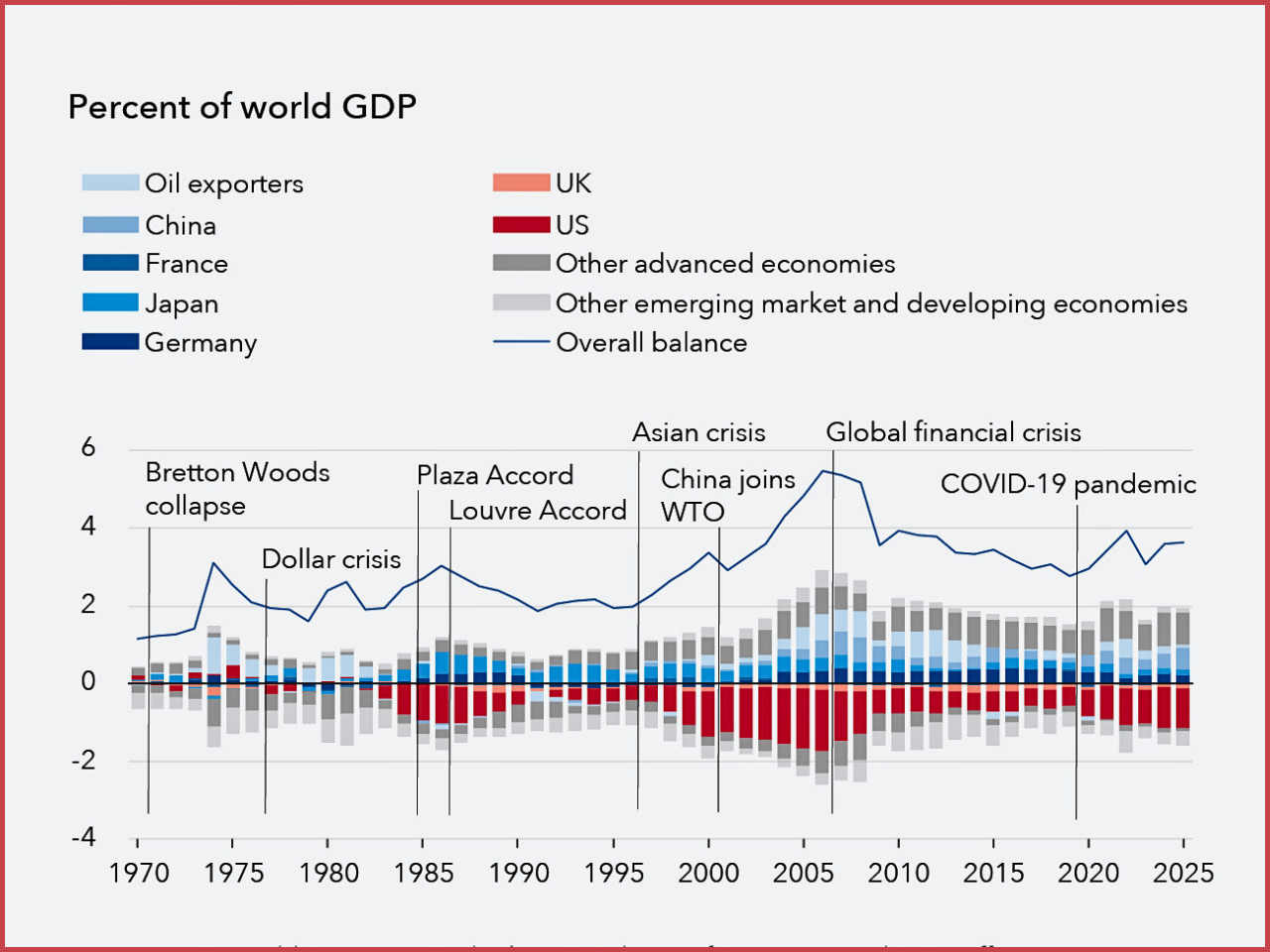

The gap in current account transactions with the rest of the world has also narrowed significantly since the global financial crisis a decade ago, the most comprehensive indicator of trade and financial transactions between a country and the rest of the world. That's all changed these days. The IMF says that the slowdown was caused primarily by “well-known macroeconomic influences," including “persistently large deficits in national saving” in the United States and China's “ongoing real estate slowdown,” which has reduced domestic demand and raised savings. This new split is serious. History suggests that a widening of imbalances is often followed by crises, sudden capital flow reversals, and major shocks to the industries and labor markets of trading partners. The world economy is grappling with a series of overlapping shocks, and any disorderly unwinding of these positions is likely to be very expensive, the IMF cautions. Much of the IMF's analysis has been directed at the constraints that are increasingly being imposed on trade restrictions, which are often argued as a way to "close trade deficits." These results confirm that, as the Fund's research has shown, tariffs tend to have small and less predictable impacts on current account balances.

The underlying principle is the reactions of the households and businesses to them. If either tariffs are seen as permanent or trading partners respond with counter-tariffs, the saving response of consumers or firms is not a meaningful one. The external balance may not be affected much, as the demand for imports may rise, but that of imports does not fall. The IMF mentions just one exception: “If the tariff is truly temporary, it can in theory induce households to save more for the future, which will increase the nation's savings.” The effects on the current account, however, are typically small and short-lived and are rarely experienced in practice. The study is presented in a timely fashion. Rising tariffs between key economies do not seem to be shrinking deficits but rather reducing output in the various parts of the world without significantly changing trade balances, and this does not provide a boost of economic growth or rebalancing. Industrial policy has also gained momentum in both advanced and emerging economies owing to strategic, security, and economic interests. The IMF makes an important distinction between two large groups and comes to very different conclusions regarding each group.

Micro-industrial policies that focus on tax incentives or subsidies for a particular firm or sector are generally less clear and less effective on external balances. Such measures, when they succeed in increasing productivity, usually increase both investment and consumption, with a negative impact on the current account. If they misallocate resources and lower the overall level of efficiency, then their external accounts could improve, but at the cost of economic output. This is not the case for macro industrial policy.

Measures that involve state-led export promotion coupled with capital flow controls, financial repression, and foreign asset accumulation can result in greater and steadier current account surpluses. But these results are not obtained by improving efficiency; they are obtained by squeezing domestic consumption and pushing national savings higher. The IMF is clear that such policies can only diminish economic welfare and are not a blueprint for sustainable growth. The IMF's preferred option rests on the old-fashioned approach to macroeconomic policy changes, which are to be implemented at the same time by both surplus and deficit countries. The Fund's scenario modeling indicates that a coordinated strategy, in which fiscal consolidation in countries with large deficits is complemented by a transition to consumption-led growth in countries with surpluses and investment to increase productivity in regions with stagnant output, could help reduce global imbalances while boosting world output.

The channels of transmission mutually reinforce each other. If China's domestic demand were to pick up, particularly in the interest rate-sensitive areas of the rest of the world, it would be easier for countries like the United States to pursue fiscal consolidation. On the other hand, a tighter fiscal stance in the U.S. would help to reduce the deflationary pressures in China and promote a structural increase in household consumption. In Europe, on the other hand, the country should be able to reap the rewards of productivity-enhancing investments that have been long overdue due to years of relative stagnation. The IMF points out that even if countries are not able to fully coordinate internationally, they shouldn't delay. The unilateral domestic adjustment is the first-best alternative for each economy assessed separately, and early action helps to minimize the risk of disorderly adjustment in the future. If delayed, the Fund warns, it will imperil national and global economic stability. The IMF expects global imbalances to further grow if trends continue. The U.S. is projected to run big deficits and have continued strong consumer spending. With limited coverage of social safety nets, China will likely keep its savings high and support its export industry handsomely. Investment and productivity growth are still weak in Europe. In this context, tariff escalation is simulated as a decrease in global production, but one that does not significantly address the underlying imbalances.

The IMF's findings come as the issue of trade policy has become an integral part of geopolitical competition. The institution's analysis does not negate the possible strategic or security goals of industrial policy or tariffs. The Fund is urging its member countries to take action on the levers that will make a difference, rather than waiting for markets to adjust.