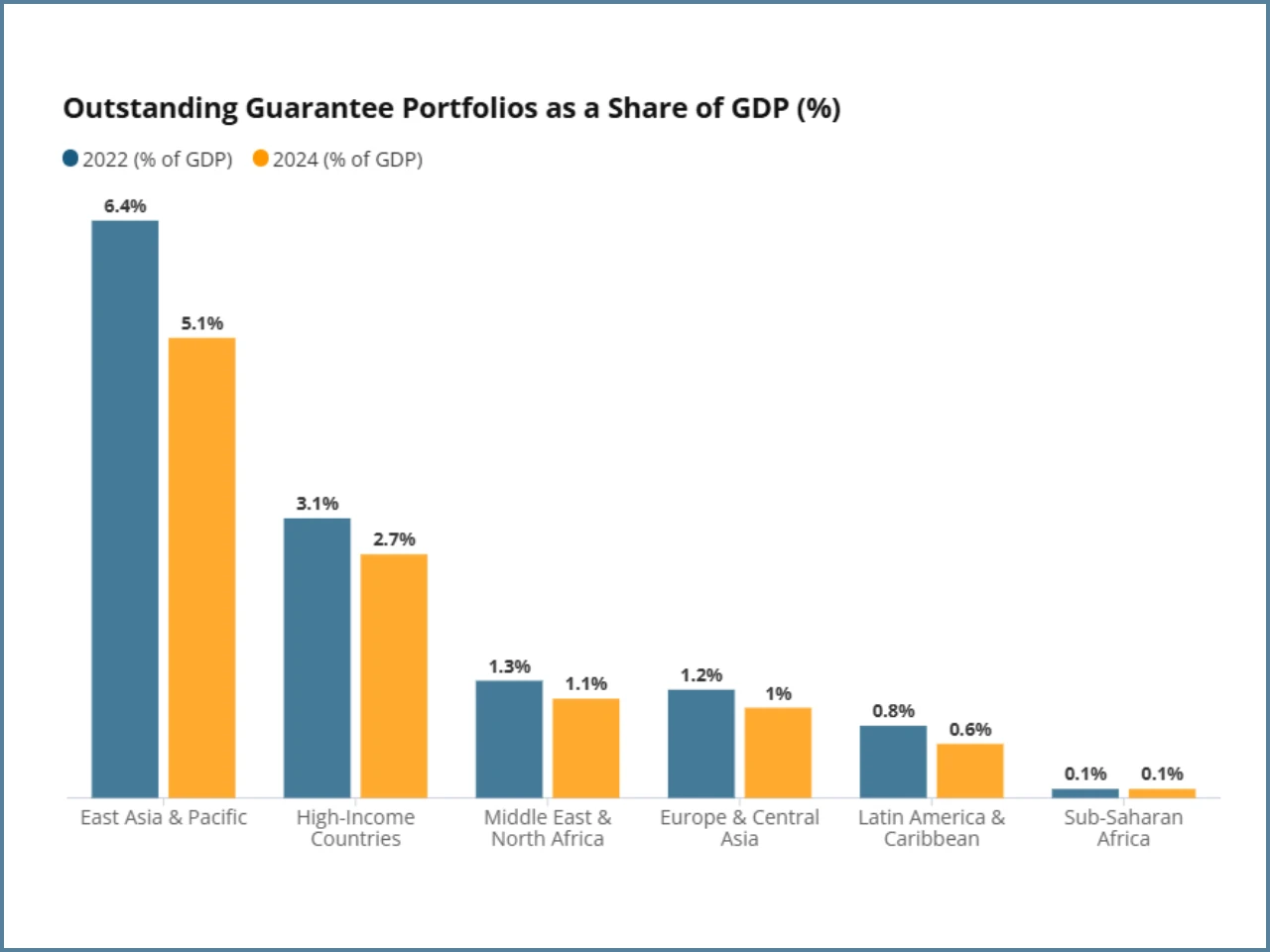

Government credit guarantee schemes are an important policy instrument for supporting small and medium enterprises (SMEs) in developing economies, as they help lower the risk of lending for banks. The survey, released by the World Bank in 108 institutions from 74 countries, exposed the magnitude and deficiencies of these programs.

The global average guarantee levels are 2% of GDP, but in Sub-Saharan Africa that is far too low at 0.1%, because that is the region’s greatest financing need.

The research has confirmed that guaranteed firms increase in size and employ more people only when the schemes reach those businesses that would have otherwise been turned down by banks.

A lot of programs do not pass this test, which is akin to subsidizing loans that would have occurred anyway. The effectiveness of a program is less dependent on the product design and more dependent on the depth and quality of the financial system and funding structure and the governance quality. Governments must push themselves to set clear objectives for improving employment, implement tougher oversight, direct more of their resources toward underserved borrowers, and devise ways to assess how public investment truly promotes to job growth.